Replace Your Workforce, Destroy Your Market: The AI Employment Data That Separates Growth From Collapse

Two numbers landed within months of each other in 2026, and together they tell a story most enterprise strategists are missing. The first: AI is already erasing 16,000 net U.S. jobs per month. The second: companies investing heavily in AI are growing headcount 10.2%, including entry-level positions at 12%. The numbers look like a contradiction. They are not. They are the same technology producing opposite outcomes based on a single variable, whether the firm deploys AI to replace humans or to augment them.

The Two Studies That Define the Debate

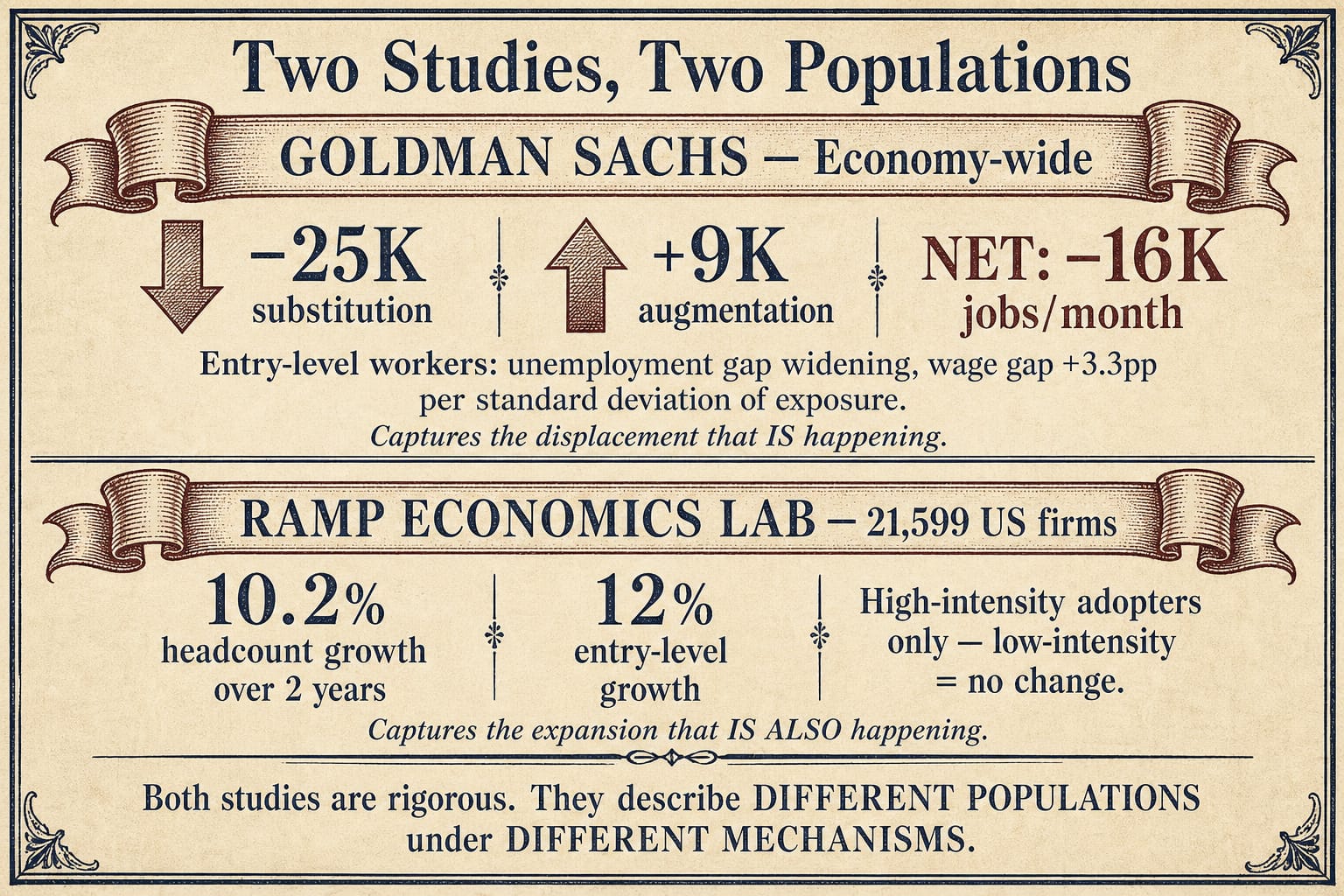

The job-loss number comes from Goldman Sachs, where economist Elsie Peng combined AI exposure scores with an IMF complementarity index to classify every occupation by whether AI substitutes for its core tasks or augments them. The finding: AI substitution eliminated roughly 25,000 jobs per month over the past year, while augmentation added back about 9,000. The net is 16,000 jobs lost per month, and the damage is concentrated. Entry-level workers face a widening unemployment gap relative to experienced workers. Each standard-deviation increase in substitution exposure widens the wage gap by 3.3 percentage points. Gen Z workers are disproportionately concentrated in the exact routine white-collar roles, data entry, customer service, and billing, that AI automates most effectively.

The growth number comes from the Ramp Economics Lab, which did something no previous study had attempted: it linked observed, firm-level AI spending, from Ramp's corporate card and bill pay data, to workforce records from Revelio Labs across 21,599 U.S. companies. The finding: firms that adopt AI grow headcount 10.2% over two years. Entry-level headcount grows 12% at the most intensive adopters. The strongest job growth occurred in the information sector, software, internet, media, and tech-adjacent firms.

Both studies are rigorous. Both use large-scale data. Both were released within months of each other. And reading them together reveals something more important than either one alone.

The Variable That Determines Which Column You Land In

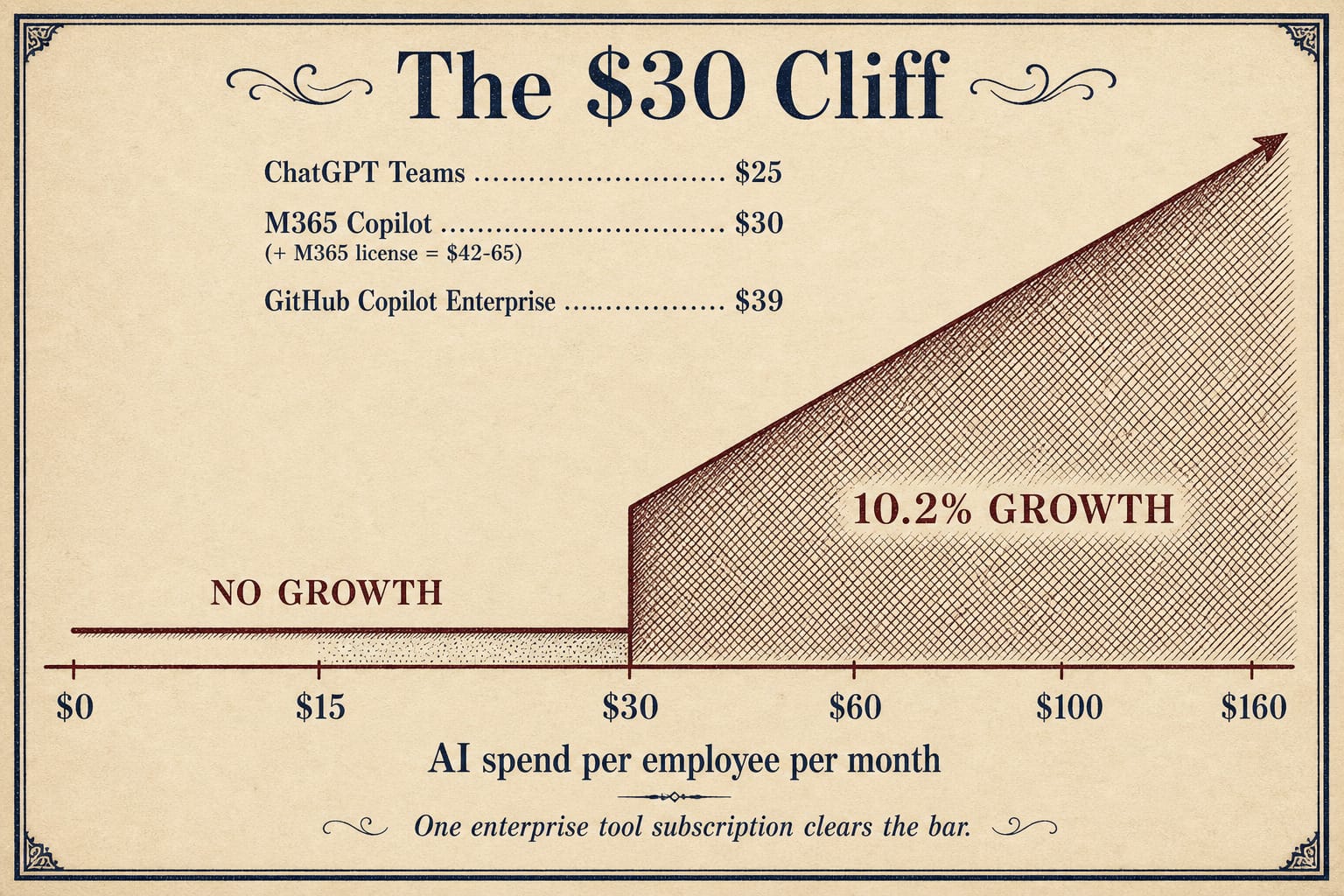

The Ramp study classifies firms as high- or low-intensity adopters based on AI spending in the first three months after adoption. The threshold is $30 per employee per month. Above that line: 10.2% headcount growth. Below it: no statistically significant change. This is not a gradient. It is a cliff.

How low is $30 per employee per month? Enterprise AI pricing data shows that a single Microsoft 365 Copilot license costs $30 per user per month, and that is before the required M365 subscription, which pushes the real cost to $42.50 to $65 or more. ChatGPT Teams is $25 per user per month. GitHub Copilot Enterprise is $39. One tool. One subscription. That is what separates "high-intensity" from "low-intensity" in the Ramp classification. The bar is not high. It is trivially low.

And yet most firms do not clear it. The companies that do were already larger, more engineering-intensive, more likely to be venture-backed, and faster-growing than the companies that do not. AI is not creating a winner-take-all dynamic. It is accelerating a winner-already-has-all dynamic, where pre-existing advantages determine who captures the gains.

This is the pattern we have been tracking at Groktopus: the economics of AI pilots show that experimentation without commitment produces nothing. The firms that reorganize work around human-AI hybrid teams, what Salesforce and Shopify have demonstrated, are the ones capturing the growth. The firms treating AI as a cost-cutting tool are the ones showing up in the Goldman data.

The Keynesian Trap Nobody Is Talking About

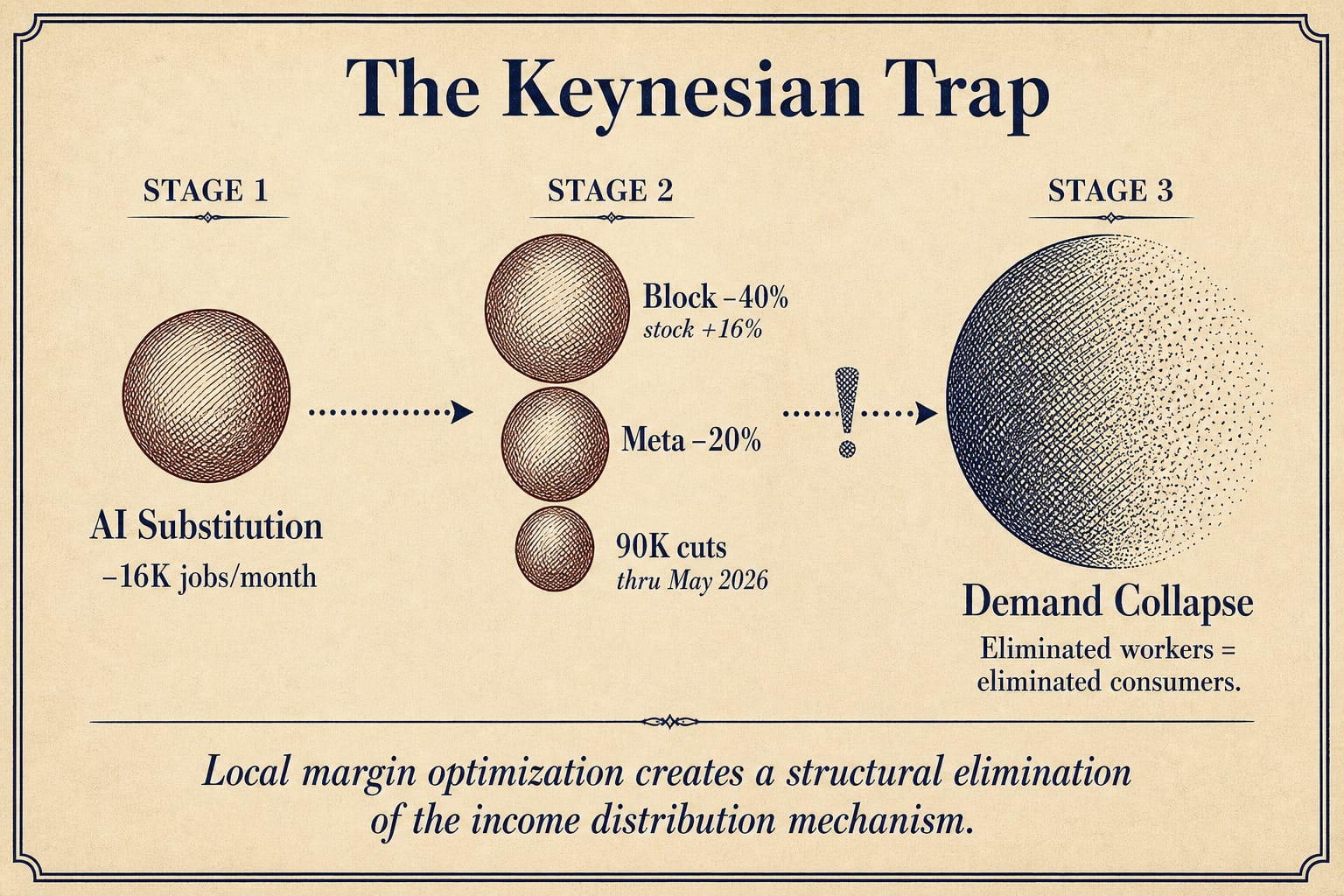

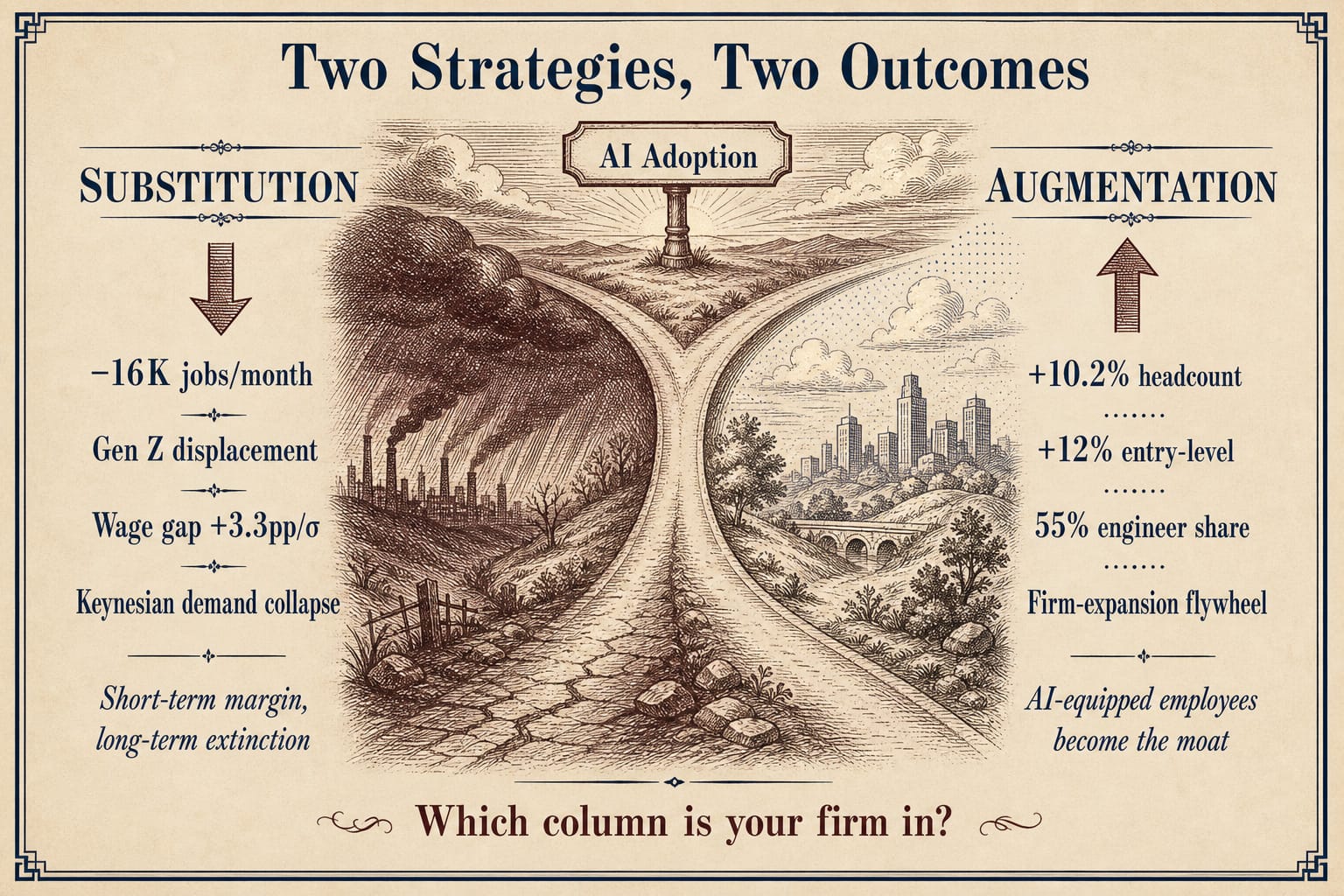

The substitution playbook is seductive because it works, locally. Block cut 40% of its workforce and saw a 24% stock surge in after-hours trading. Meta saw the signal and began planning a 20% cut within weeks. Through May 2026, nearly 90,000 job cuts were tied to AI. Every one of those eliminated workers was also an eliminated consumer. Multiply that across the economy and the math stops working, not eventually, but quickly. Firms produce more goods while fewer consumers can afford to buy them. This is not a recession. It is a structural elimination of the income distribution mechanism. The companies racing to replace workers are solving a local optimization while creating a global catastrophe.

The augmentation playbook avoids this trap entirely, but not through charity. It avoids it because AI makes a firm's output cheaper, which makes expansion rational, which requires more humans. Lower production costs in software, documentation, customer support, and internal tooling raise the return on expanding the whole firm, not just the engineering team. The Ramp data confirms this mechanism is real: headcount rose across engineering, sales, administration, customer service, finance, and marketing. This is not redistribution of surplus. It is reinvestment for growth.

Engineering Was Supposed to Be First

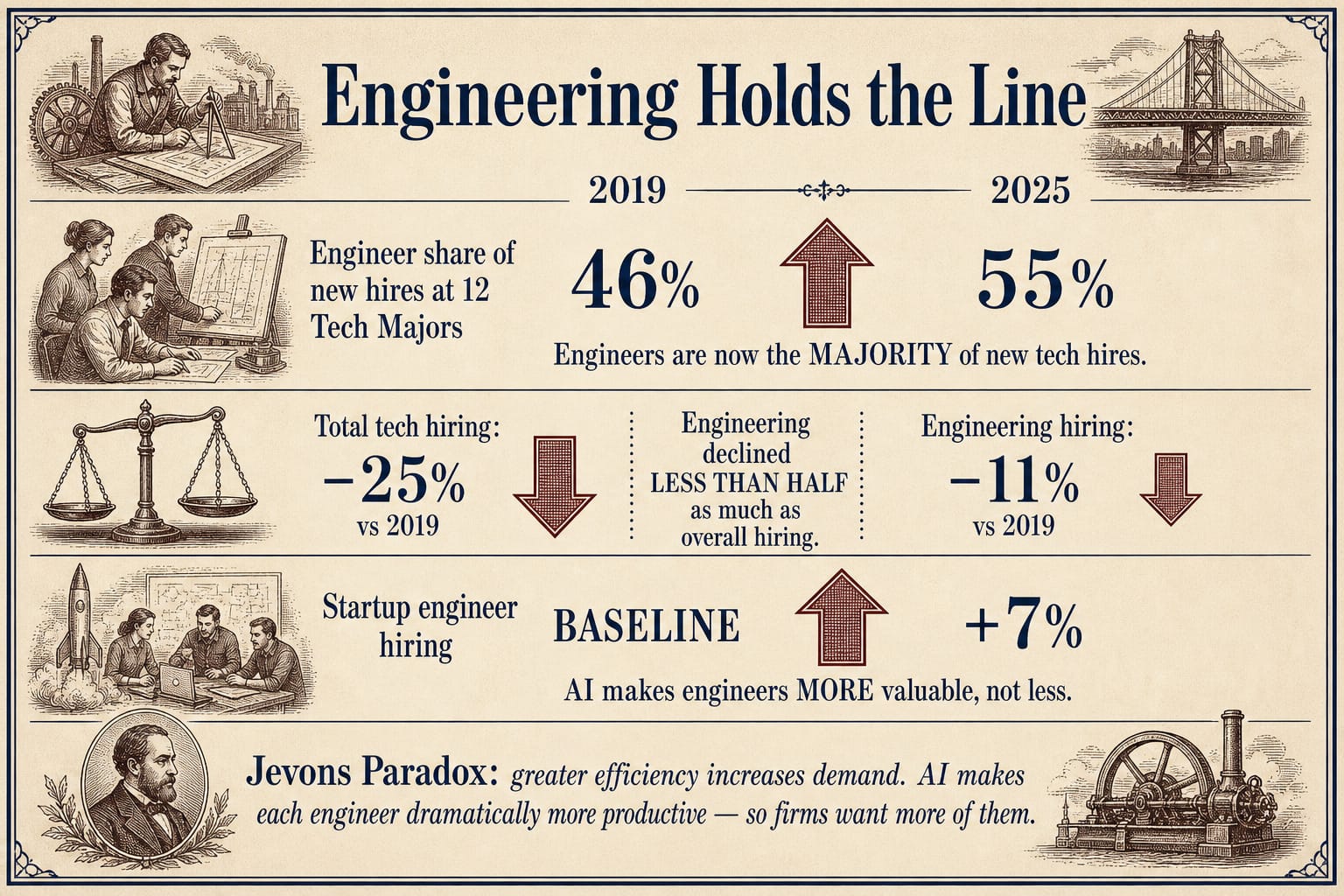

If AI were going to eliminate a profession, software engineering should have been the canary. AI coding tools are the most visibly capable category of AI application. They write code, debug, refactor, generate tests. Every major tech company has integrated them. And yet SignalFire's State of Talent Report, which tracked millions of employee records across more than 80 million companies, found that engineering was the most resilient job function in 2025.

Total hiring across large tech companies dropped 25% compared to 2019 levels. Engineering hiring declined only 11%. Engineers comprised 55% of all new hires at the twelve Tech Majors in 2025, Alphabet, Meta, Apple, Amazon, Microsoft, Netflix, Nvidia, Tesla, Uber, Airbnb, Block, and Stripe, up from 46% in 2019. Early-stage startups hired 7% more engineers in 2025 than in 2019. Nvidia CEO Jensen Huang, whose engineers have deeply integrated agentic AI into their workflows, said it directly: "Somebody said that AI is going to destroy all of the software engineering jobs." His counter: "Software engineers are busier than ever."

This is a textbook Jevons paradox. Greater efficiency in using a resource does not reduce demand for it, it increases demand, because the work expands to fill the new capacity. AI makes engineers dramatically more productive per hour. The rational firm response is not fewer engineers. It is more engineering.

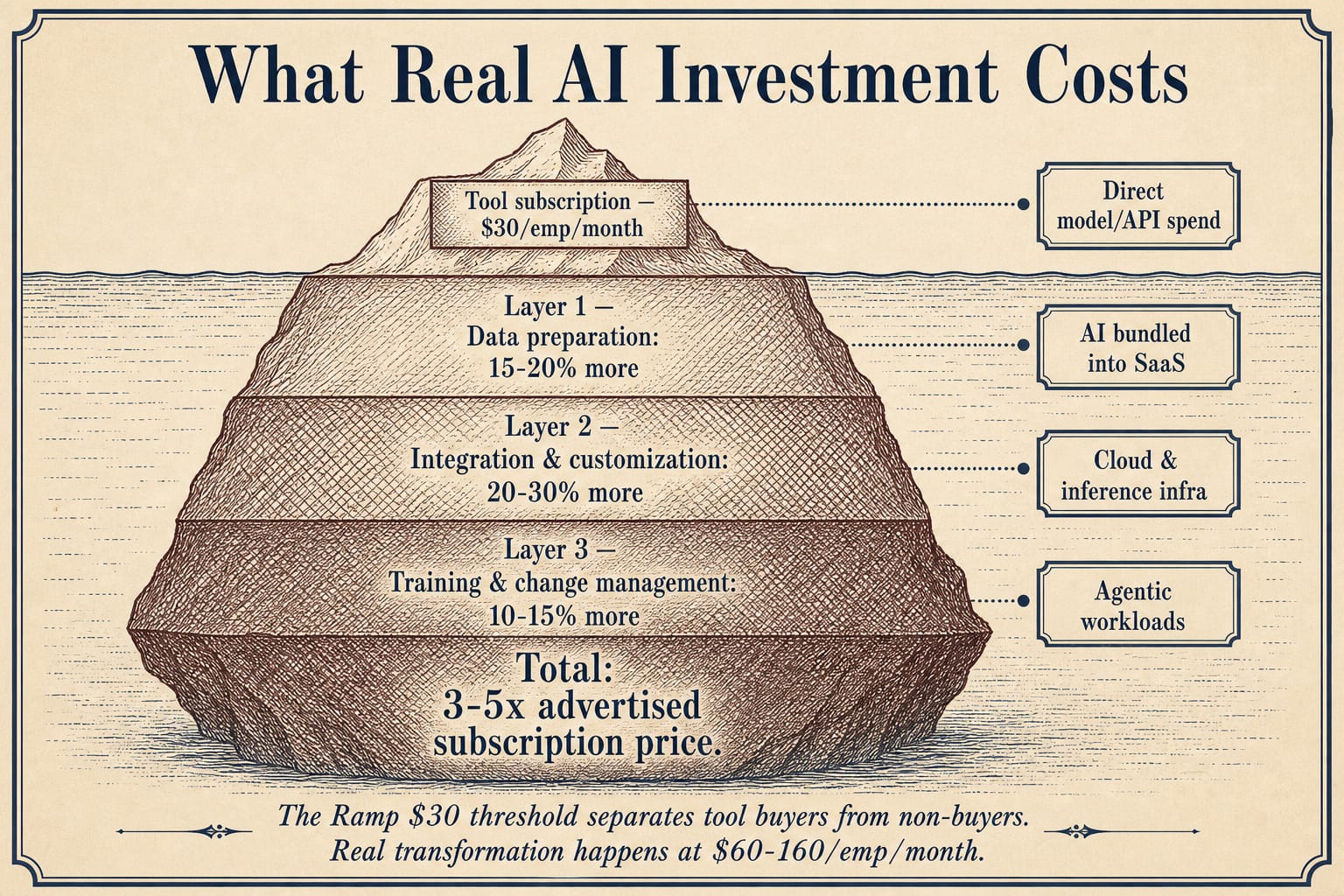

The $30 Trap

So what does real AI investment actually cost? The $30 per employee per month threshold is not the marker of a serious AI transformation. It is the marker of having bought at least one tool. Enterprise AI spending benchmarks show that mid-size organizations investing seriously in AI spend $60 to $160 per employee per month across tooling, infrastructure, training, and process redesign, and enterprise implementations cost multiples of the advertised subscription price when accounting for data preparation (15 to 20% of budget), integration and customization (20 to 30%), and training and change management (another 10 to 15%).

The Ramp threshold does not separate companies doing AI right from companies dabbling. It separates companies that signed up for one enterprise AI tool from companies that did not. The real divergence, the 10.2% headcount growth, belongs to the firms spending multiples of the threshold across all four layers of AI cost: direct model and API spend, AI bundled into existing SaaS, cloud and inference infrastructure, and agentic workloads. Those are the firms where AI actually changes the unit economics enough to make expansion rational.

Most firms will never cross that line. They will buy the Copilot licenses, run the pilots, and see no statistically significant change, in headcount, in productivity, in market position. Meanwhile, the firms that already have the capital, the technical staff, and the organizational readiness to deploy AI deeply will pull further ahead. The gap is not between AI adopters and non-adopters. It is between transformation investors and tool buyers.

The Choice

The data does not debate which view of AI is correct. It shows which strategy survives. One strategy, replace humans, capture the surplus, reward shareholders, produces the Goldman numbers. Sixteen thousand jobs lost per month. Gen Z displacement. Widening wage gaps. And a Keynesian trap that collapses demand from the very consumers whose purchasing power the strategy eliminates.

The other strategy, augment humans, expand the firm, build the moat, produces the Ramp numbers. Ten percent headcount growth. Entry-level hiring at 12%. Engineers busier than ever. AI-equipped employees who are more productive, more creative, and more valuable than either humans alone or AI alone.

The uncomfortable implication is that most enterprises do not get to choose which strategy they pursue. Their existing resources, their capital reserves, their technical staff depth, their organizational readiness, have already made the choice for them. The firms positioned to choose augmentation were growing faster before they adopted AI. The firms defaulting to substitution are absorbing the displacement. AI accelerates the divergence that was already underway.

The question for enterprise strategists is not "which study is right?" It is "which column is your firm in, and what are you doing to cross the line?"