The Compression Ceiling: Why AI Nano-Unicorns Can't Stay Nano

Cal AI reached $21 million in annual revenue with two people in ten months. No sales team. No marketing department. No customer success organization. Just one founder and one collaborator, building and selling an AI product that would have required a 50-person company five years ago.

That sentence reads like an unbelievable hypothetical in 2023. It's a verified data point in 2026.

The race to document the nano-unicorn has become a cottage industry. Eze Vidra at VC Cafe coined the term and catalogued the outliers. Ben Lang's TinyTeams directory tracks them. Sam Altman and Dario Amodei have placed public bets on when the first one-person billion-dollar company will appear.

The evidence is real, measurable, and accelerating. But there's a structural pattern beneath the headlines the hype cycle is missing. The nano-unicorns are real. They are also temporary. The tension between those two facts is what the data actually shows.

Act I: The Compression Is Real

Let's start with the companies that prove the thesis. These aren't hypotheticals. They're documented businesses with named founders, verified revenue, and in several cases, SEC-adjacent filings.

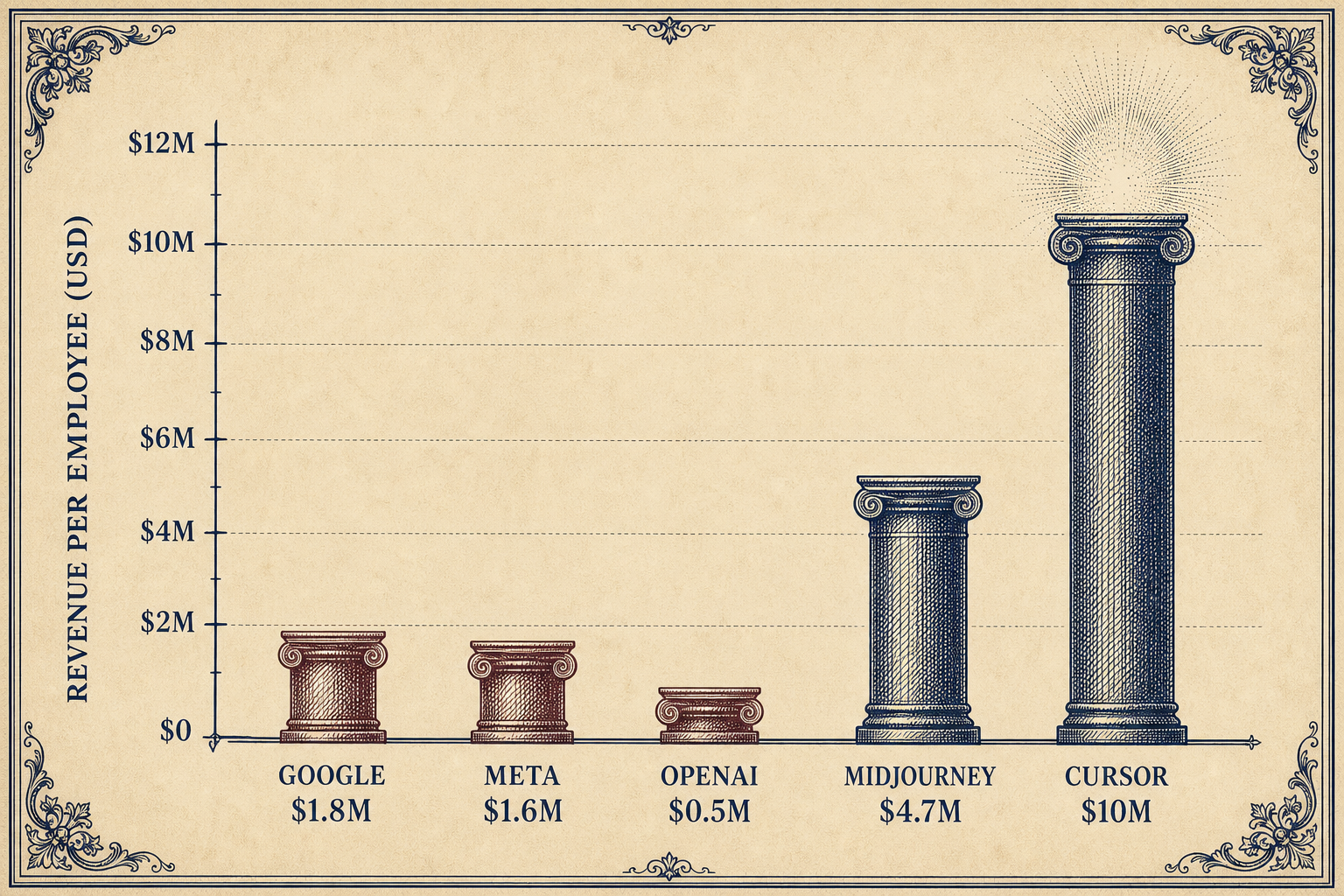

Midjourney hit an estimated $500 million in annual revenue with roughly 107 employees. That's about $4.7 million per employee. For context: Google generates about $1.8 million per person. Meta does $1.6 million. OpenAI, the poster child of the AI boom, runs at roughly $500,000. Midjourney's ratio more than doubles the most efficient big-tech company in existence. And they did it with zero venture capital, zero marketing spend, and a product that launched as a Discord bot.

Cursor (Anysphere) hit $100 million in annual recurring revenue in January 2025 with roughly 20 employees and zero marketing budget. By May 2026, they had crossed $3 billion in ARR. That's the fastest B2B SaaS scaling in history. Their free-to-paid conversion rate of 36% (compared to the typical 2-5% freemium benchmark) meant the product sold itself so effectively that the company deliberately made it hard for enterprises to buy it: they removed contact forms from their website until thousands of companies per month were reaching out unsolicited.

Consider the broader field. Gamma operates with 28 employees serving 50 million users. ElevenLabs crossed $500 million ARR with fewer than 100 people. Cal AI we already covered: 2 people, $21 million ARR, 10 months. MAGNIFIC: 2 people, $10 million ARR, 1 year. Lovable: roughly 15 people, $100 million-plus ARR, under two years.

The data is consistent enough across enough companies that it demands to be taken seriously. AI tooling has collapsed the time and headcount required to reach product-market fit. A two-person team in 2026 can ship and scale what required a 20-person team in 2022.

Act II: The Ceiling They All Hit

Here's the finding that changes the narrative. Every nano-unicorn that crossed the $500 million ARR threshold had to hire significantly.

Cursor went from roughly 20 people at $100 million ARR to roughly 300 people at $3 billion ARR. Revenue grew 30x; headcount grew 15x. The revenue-per-employee ratio remains extraordinary at $10 million per person. But the company is no longer a nano-unicorn in any meaningful sense. They have an enterprise sales team they had to acqui-hire from an existing CRM startup. They have compliance, security, and model training infrastructure teams that didn't exist at 20 people.

Midjourney went from roughly 11 people at their early stage to around 107 today. Revenue roughly doubled from $200 million to $500 million ARR. Headcount grew 10x. They now have dedicated legal, finance, and compliance staff. The founder who personally negotiated Meta's IP licensing deal can't be the only deal-closer anymore.

The pattern is consistent. Extreme compression works at the early stage but breaks at scale. The mechanisms aren't mysterious:

Enterprise sales requires human trust transfer that a landing page and chatbot can't replace. At a certain revenue threshold, deals get large enough that counterparties need a person who will be accountable.

Institutional procurement compliance (banking relationships, insurance requirements, regulatory filings, vendor qualification) demands dedicated attention that compounds with revenue, not headcount.

Coordination debt. Three people have three communication channels. Three people managing AI systems across sales, product, and compliance create nine coordination surfaces. At some point, the meta-work of managing the AI toolchain exceeds what anyone can do as a side task.

Burnout has no redundancy in a 3-person company. There is no backup. There is no succession. There is no one to absorb load when one role overwhelms its occupant.

The honest caveat: the sample size is small. We have maybe 20 companies that have demonstrated extreme compression at meaningful scale. The ceiling may be an artifact of limited data rather than a structural law. And the ceiling is almost certainly rising. As AI agent capabilities, tooling maturity, and institutional adaptation accelerate, what requires 300 people today may require 50 in 2028.

But the best data we have today says the same thing: cross $500 million ARR, and you will hire.

Act III: Where the Ceiling Breaks, and Where It Doesn't

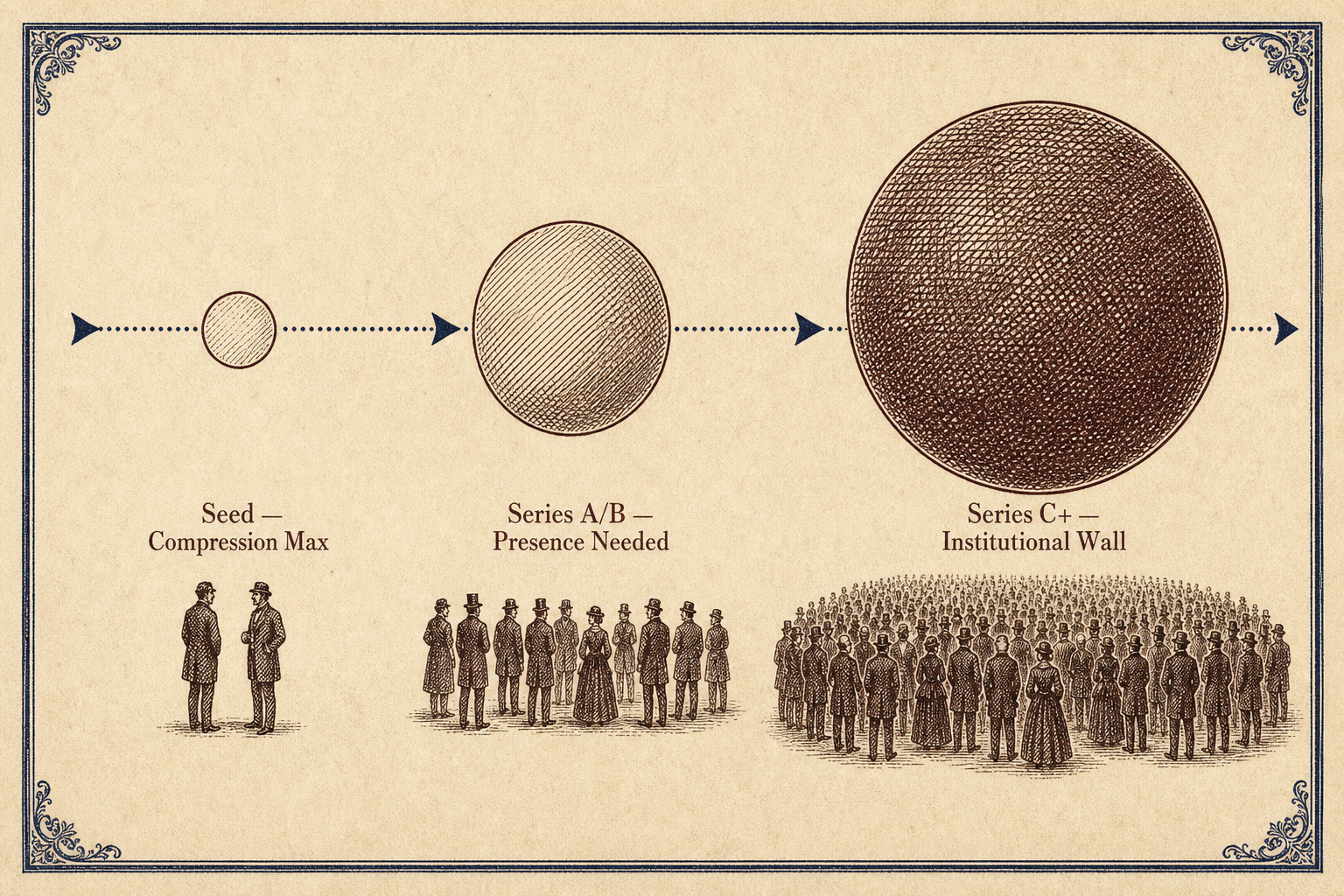

The most useful way to think about the compression ceiling is tied to the funding stages your board already tracks.

Seed stage offers the purest compression advantage. That $21 million in ARR from a 2-person team changes the math entirely. You can reach meaningful revenue with negligible capital. The traditional seed pitch ("give us $2 million to hire 10 engineers") is being replaced by ("give us $500,000 to scale our AI infrastructure"). At this stage, the compression edge is maximal.

By Series A to B, the question shifts from "can you build it" to "can you sell it." This is where the Presence function becomes critical. Enterprise deals at this stage require someone who can be in a room. The compressed team's advantage narrows. It hasn't disappeared.

At Series C and beyond, the institutional wall becomes binding. Banking relationships, D&O insurance, regulatory compliance, and Fortune 500 procurement rules all demand a level of organizational infrastructure that a 5-person team can't credibly provide. The company can still be far leaner than historical benchmarks. But it cannot be five people.

The practical implication for enterprise decision-makers: compression gives you an advantage in speed and capital efficiency through the growth phase. Plan for organizational scaling when you hit the institutional wall. The companies that navigate this successfully treat compression as a phase, not a permanent operating model. They build the organizational infrastructure their future revenue will demand.

The Counterargument That Makes This Honest

The 11x story is the necessary cautionary tale. Backed by Andreessen Horowitz and Benchmark with $75 million in funding, the London-based AI sales automation startup was caught fabricating customer logos, inflating ARR by roughly 10x, and sustaining 70-80% churn during trial periods. The product, "AI digital workers," was barely functional. Hallucinations. Email delivery failures. Culture described as toxic: 80-hour weeks, employees sleeping in the office, the founder publicly shaming staff.

The 11x case doesn't invalidate the compression thesis. It exposes its vulnerability. When revenue targets exceed what a compressed team can sustainably deliver, the temptation to fabricate is enormous. The same speed that lets a 3-person company ship product in a week also lets it ship misleading numbers. Compression culture without accountability infrastructure is a fraud vector.

What This Means for Your Strategy

The nano-unicorn era is real. Two-person companies generating $21 million in revenue aren't a thought experiment. They're a verified outcome of the AI era. That compression will deepen as agent capabilities improve and institutional infrastructure adapts.

But the fantasy of a permanent 3-person billion-dollar company, three people holding down the irreducible functions forever, never hiring, never scaling, doesn't survive contact with the data we have today. The companies that have crossed the $500 million threshold all hired. The sample is small. The ceiling is rising. The story in 2028 may look completely different from the story in 2026.

As of now, the signal is clear.

Build as small as you can for as long as you can. Then build the organizational infrastructure your future revenue will require, before you need it. The nano-unicorn is a phase. The company that survives it is the real prize.

Sources

CNBC — Cursor Series D Coverage

ProductGrowth Blog — Midjourney

Carta — Founder Ownership Report 2025

IndieHackers — Nano-Unicorn Roundup